Learn how to finance a car through State Farm and get competitive rates and flexible payment options. Start your application process today!

If you’re in the market for a new car, financing is often a necessary step in the purchasing process. State Farm offers a variety of options for financing your vehicle, but navigating the process can be overwhelming. Fortunately, with a little knowledge and preparation, you can secure the financing you need with ease. So, whether you’re a first-time car buyer or an experienced driver looking to upgrade, State Farm has you covered. Let’s dive into the world of car financing and explore some tips and tricks to make the process as smooth as possible.

State Farm is one of the largest automobile insurance providers in the country that also offers loans for car financing. Financing a car through State Farm is an easy and convenient process that allows you to get the car of your dreams without breaking the bank. In this article, we will guide you through the process of getting a car loan through State Farm.

Step 1: Check Your Credit Score

The first step to financing a car through State Farm is to check your credit score. A good credit score will help you get better loan terms and lower interest rates. You can check your credit score for free online from various websites such as Credit Karma or Annual Credit Report.

Step 2: Determine Your Budget

Before applying for a car loan, it is important to determine your budget. Consider your monthly income, expenses, and any down payment you plan on making. State Farm offers a car loan calculator on their website that can help you determine your monthly payment based on the loan amount, interest rate, and term.

Step 3: Apply for a Loan

Once you have determined your budget, you can apply for a car loan through State Farm. You can apply online or visit a local State Farm agent to fill out an application. You will need to provide personal information such as your name, address, employment information, and social security number.

Step 4: Get Pre-Approved

Getting pre-approved for a car loan through State Farm is a great way to know how much you can afford and what your interest rate will be. Pre-approval also makes the car buying process easier and faster. You can get pre-approved online or through a local State Farm agent.

Step 5: Choose Your Car

Once you have been approved for a car loan, you can start looking for your dream car. State Farm offers financing for both new and used cars. You can buy a car from a dealership or a private seller. It is important to do your research and find a car that fits your budget and needs.

Step 6: Negotiate the Price

When buying a car, it is important to negotiate the price. This can save you money in the long run. You can use your pre-approved loan amount to negotiate with the seller. State Farm also offers a car buying service that can help you find the right car at the right price.

Step 7: Finalize the Loan

Once you have chosen your car and negotiated the price, you will need to finalize the loan. This involves signing the loan agreement and any other necessary documents. You will also need to provide proof of insurance before you can drive off with your new car.

Step 8: Make Payments

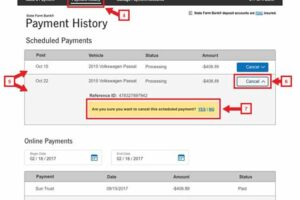

After finalizing the loan, it is important to make your monthly payments on time. Late payments can result in fees and damage your credit score. State Farm offers various payment options such as online payments, automatic payments, and payments by phone.

Step 9: Refinance Your Loan (Optional)

If you find that your interest rate is too high or your monthly payments are too much, you can consider refinancing your car loan. Refinancing can help you get a lower interest rate and reduce your monthly payment. State Farm offers refinancing options for existing car loans.

Step 10: Pay Off Your Loan

Congratulations! You have successfully financed your car through State Farm. Once you have made all the necessary payments, you will own your car outright. This is a great feeling and a big accomplishment. You can then decide to keep your car or sell it and use the proceeds towards a new car.

Financing a car through State Farm is a great way to get the car of your dreams at an affordable price. Follow these steps and you will be on your way to owning a new car in no time.

Financing a car through State Farm is a convenient and hassle-free way to get behind the wheel of your dream car. With a variety of auto loan options available, State Farm offers competitive rates and flexible payment terms to suit your budget and lifestyle. In this article, we will explore the benefits of financing a car through State Farm, what you’ll need to apply, the impact of your credit score on financing, the types of auto loans available, how to apply for a loan, the approval process, reviewing the loan terms and signing the agreement, frequently asked questions, and, finally, how State Farm makes car financing easier for you.

One of the biggest benefits of financing a car through State Farm is that you can get pre-approved for an auto loan before even going to the dealership. This means that you’ll know exactly how much you can afford to spend on a car, which can save you time and money in the long run. Additionally, State Farm offers competitive rates and flexible payment terms, so you can choose a loan that works best for your budget and financial goals.

Before applying for an auto loan with State Farm, you’ll need to gather some important information. This includes your personal information (such as your name, address, and social security number), employment information (such as your employer’s name and your job title), and financial information (such as your income and monthly expenses). You’ll also need to provide information about the car you want to buy, including the make, model, and year.

Your credit score plays a significant role in determining whether or not you qualify for an auto loan, as well as the interest rate you’ll be offered. A higher credit score typically means a lower interest rate, which can save you money over the life of the loan. It’s important to check your credit score before applying for a loan, and to take steps to improve it if necessary.

State Farm offers several types of auto loans, including new car loans, used car loans, and refinancing loans. New car loans are available for cars that are less than two years old, while used car loans are available for cars that are up to ten years old. Refinancing loans are available for those who want to refinance an existing auto loan.

To apply for a State Farm auto loan, you can start by visiting their website and filling out an online application. You’ll need to provide the information mentioned earlier, as well as information about the car you want to buy. After submitting your application, you’ll receive a decision within a few business days.

The approval process for a State Farm auto loan is fairly straightforward. After reviewing your application, State Farm will determine whether or not you qualify for a loan based on factors such as your credit score and income. If you are approved, you’ll receive an offer letter outlining the terms of the loan, including the interest rate, loan amount, and repayment period.

Before signing the loan agreement, it’s important to review the terms carefully and make sure you understand them. This includes the interest rate, monthly payment amount, and any fees or penalties associated with the loan. Once you’re comfortable with the terms, you can sign the agreement and move forward with your purchase.

If you have any questions about financing a car through State Farm, there are several frequently asked questions on their website that can help. These include questions about the application process, eligibility requirements, and repayment options. If you still have questions, you can also contact a State Farm representative directly for assistance.

In conclusion, financing a car through State Farm is a convenient and hassle-free way to get behind the wheel of your dream car. With a variety of auto loans available, competitive rates, and flexible payment terms, State Farm makes it easy to find a loan that works for you. By understanding the application process, the impact of your credit score on financing, and the types of loans available, you can make an informed decision and get the best possible loan for your needs.

Financing a car can be a daunting task, but with State Farm, the process can be made simple and stress-free. Here’s a step-by-step guide on how to finance a car through State Farm:

- Contact your local State Farm agent: The first step in financing a car through State Farm is to contact your local agent. They will help you understand the financing options available and answer any questions you may have.

- Complete a loan application: Once you’ve decided on a financing option, you’ll need to complete a loan application. This can be done online or in-person with your agent. You’ll need to provide information such as your income, employment status, and credit score.

- Get pre-approved: After submitting your loan application, you’ll receive a pre-approval decision from State Farm. This will let you know how much you’re approved to borrow and what your interest rate will be.

- Find your car: Now that you’re pre-approved, it’s time to find your dream car. You can shop around at different dealerships or look for private sales. Keep in mind the amount you’re approved to borrow and choose a car that fits within your budget.

- Finalize the loan: Once you’ve found your car, you’ll need to finalize the loan with State Farm. This includes providing information about the vehicle, such as the make, model, and VIN number. You’ll also need to provide proof of insurance.

- Make your payments: With your loan finalized, it’s time to start making your payments. State Farm offers flexible payment options, including automatic payments and online bill pay. Be sure to make your payments on time to avoid late fees and damage to your credit score.

Financing a car through State Farm is a great option for those looking for a simple and easy way to get behind the wheel of their dream car. With competitive interest rates and flexible payment options, State Farm can help you get the car you want at a price you can afford.

So why wait? Contact your local State Farm agent today and start your journey towards owning your dream car!

Thank you for taking the time to read about financing a car through State Farm. We hope that this article has been informative and helpful in your search for the perfect vehicle. As you know, purchasing a car is a major investment, and it’s important to make sure that you have the right tools and resources at your disposal to make an informed decision.

State Farm offers a number of options for financing your car, whether you’re buying new or used. With competitive rates and flexible terms, you can find a payment plan that works for your budget and lifestyle. And because State Farm is a trusted name in insurance and financial services, you can feel confident that you’re getting a quality product from a reputable company.

When it comes to financing a car through State Farm, there are a few things to keep in mind. First, be sure to do your research and shop around to find the best deal. Compare rates from multiple lenders, including State Farm, to ensure that you’re getting the most competitive offer. And don’t forget to factor in other costs, such as insurance, taxes, and maintenance, when calculating your monthly payments.

Overall, financing a car through State Farm can be a smart choice for many consumers. With a variety of options and competitive rates, State Farm makes it easy to get behind the wheel of your dream car. So, what are you waiting for? Contact your local State Farm agent today to learn more about how you can finance your next vehicle!

.

When it comes to financing a car, State Farm is one of the options that people consider. Here are some common questions that people also ask about how to finance a car through State Farm:

- What types of vehicles can be financed through State Farm?

- What are the interest rates for State Farm car loans?

- How do I apply for a State Farm car loan?

- What documents do I need to apply for a State Farm car loan?

- How long does it take to get approved for a State Farm car loan?

- What happens after I am approved for a State Farm car loan?

State Farm offers financing for new and used cars, trucks, SUVs, vans, and motorcycles.

Interest rates vary depending on several factors, including credit score, loan amount, and loan term. However, State Farm offers competitive rates for both new and used car loans.

You can apply for a State Farm car loan online, over the phone, or in person at a State Farm agent’s office. You will need to provide personal and financial information, as well as information about the car you want to finance.

You will need to provide proof of income (such as pay stubs or tax returns), proof of insurance, and proof of identity (such as a driver’s license or passport).

The approval process can take anywhere from a few minutes to a few days, depending on the complexity of your application and the amount of information you need to provide.

You will receive the loan funds directly from State Farm, which you can use to purchase the car. You will then make monthly payments to State Farm until the loan is paid off.

Overall, financing a car through State Farm can be a convenient and competitive option for those in need of a car loan. With flexible terms and competitive interest rates, it’s worth considering as part of your car-buying process.